Quick Thought: Company "Option" Value

Happy New Year + Company Value Breakout with Real Options and Why TSLA is Overvalued

Happy New Year to all of you!

My plan for 2022 is to provide more frequent content that you will find practical, actionable, and valuable.

Thanks for being a reader of this *short* but growing newsletter. I hope you can share the articles with fellow value investors.

Company “Real Option” Value

If you haven’t read the latest version of Expectations Investing by Michael Mauboussin and Alfred Rappaport, you NEED to pick up a copy.

The premise of the book is to help investors understand and extrapolate the assumptions inherent in the stock price of a company. Effectively reverse engineering the assumptions implied by analyzing a company’s stock price.

One concept discussed in the book is the idea of breaking up a company’s value into two values:

The current business value (ongoing operations); and,

A real option value. A real option is defined as an option that exists to a business to expand, extend, or abandon a project. A project is usually a new business opportunity that a company has available to them through current investments or resources at their disposal.

This is not a new concept, however, it is a highly important concept and the authors provide a practical framework to use this type of analysis. This analysis can provide investors with a tool to understand the gap between value and price as this gap can be explained the markets expectation of real options available to the company.

TESLA

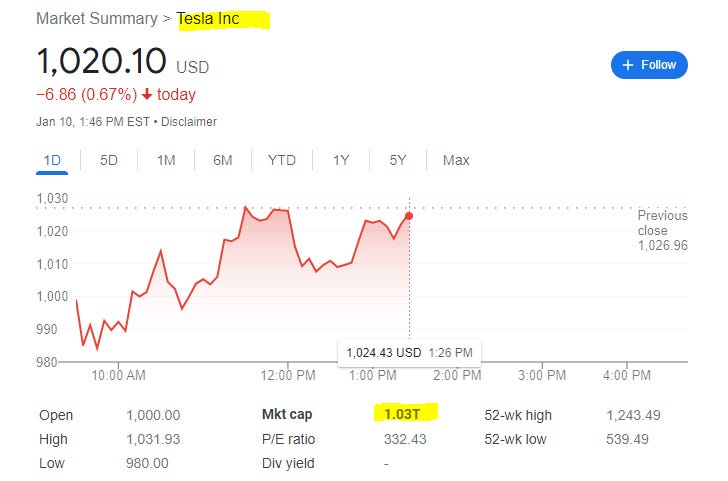

Let’s use Tesla (TSLA) as an example - And see why I think their “real option” is overvalued. The company currently reports a $1 Trillion market cap (as of 1/10/2022).

Aswath Damodaran’s recently valued Tesla with an equity value of $640 billion - let’s use his value for now. This captures Tesla’s current business of manufacturing and selling cars and building and installing solar systems under Solar City. You can read his article to understand his assumptions - they are generous.

We can derive an estimated option value of the remaining business from the market by simply subtracting our determination of value ($640B) from the current market capitalization ($1T).

$1 Trillion - $640 Billion = $360 Billion

The $360 billion represents the “real option” value implied by the market. The market is pricing in a real option consisting of all the potentially valuable business avenues Tesla might pursue such as autonomous taxis, semi-trucks, licensing vehicle technology, selling EV batteries, vehicle insurance, etc. Investors are expecting Tesla to pursue many “real options” which is why the price eclipses many of its competitors.

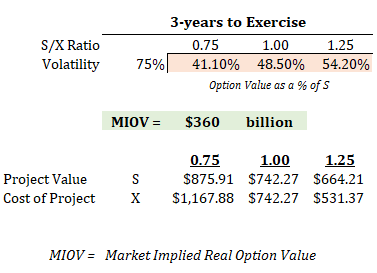

Armed with the market implied real option of $360 billion, we can make some simple assumptions using option analysis. (The book goes deeper, so I suggest you read it for a better technical understanding)

Based on the analysis from the book, we can extrapolate assumptions from the market implied option value and then run through a reasonableness test.

Let’s make a few assumptions:

Let’s use Tesla’s historical price volatility of 75% for our option calculations;

Let’s assume Tesla has approximately 3 years to exercise these options - Competition and a change in market dynamics does not allow real options to live forever; and,

Let’s do some sensitivity analysis, assuming that the cost of these projects (X) exceeds (.75), equal to (1.0), and is less than (1.25) then the projects value (S) which is present value of the projects incremental cash flows (S). (For example, the .75 means that the value of the project is currently 75% of the total value of the project - which implies it fails the NPV test. However, there is still option value as the expected cash flows may increase as time increases.)

Overall Results

We can answer two questions from the above analysis:

How large does the project value (S) have to be to justify an imputed $360 billion real options value?

How large is the potential real options exercise cost (X) that justifies a $360 billion real options value?

Scenario 1 - 0.75 Value (S)-to-Cost (X) Ratio

The 0.75 means that the value of the project (S) is 75% of the cost (X) as of today. This means that it is not a worthwhile project as it fails the NPV test. However, there is still value since the expected future cash flows (i.e. project value), which is S, may change between now and option expiration.

Let’s answer the questions for this scenario:

For Tesla to command a $360 billion option value, the project value (S) must be worth at least $875 billion. As an analyst, you can now decide if the magnitude of this market opportunity is reasonable given all the possible avenues they can pursue. Project value is the present value of all cash flows from these projects.

For Tesla to command a $360 billion option value, the exercise cost (X) must be at least $1.2 trillion. In the past 4 years Tesla has spent approximately $19.8 billion on capital expenditures and R&D - or approximately 1.6% of the cost of the possible opportunities. This implies Tesla would need to spend substantially more ($1 Trillion at least) to achieve the option value.

Scenario 2 - 1.00 Value (S)-to-Cost (X) Ratio

The 1.00 means that the value of the project (S) is equal to 100% of the cost (X) as of today. This means that it has an NPV of 0. However, there is still value since the expected future cash flows (i.e. project value), which is S, may change between now and the option expiration.

Let’s answer the questions for this scenario:

For Tesla to command a $360 billion option value, the project value (S) must be worth at least $742 billion. As an analyst, you can now decide if the magnitude of this market opportunity is reasonable given all the possible avenues they can pursue. Project value is the present value of all cash flows from these projects.

For Tesla to command a $360 billion option value, the exercise cost (X) must be at least $742 billion. In the past 4 years Tesla has spent approximately $19.8 billion on capital expenditures and R&D - or approximately 2.6% of the cost of the possible opportunities. Again, this implies Tesla would need to spend substantially more to achieve the option value.

Scenario 3 - 1.25 Value (S)-to-Cost (X) Ratio

The 1.25 means that the value of the project (S) is equal to 125% of the cost (X) as of today. This means that the projects have positive NPV’s.

Let’s answer the questions for this scenario:

For Tesla to command a $360 billion option value, the project value (S) must be worth at least $664 billion. As an analyst, you can now decide if the magnitude of this market opportunity is reasonable given all the possible avenues they can pursue. Project value is the present value of all cash flows from these projects.

For Tesla to command a $360 billion option value, the exercise cost (X) must be at least $531 billion. In the past 4 years Tesla has spent approximately $19.8 billion on capital expenditures and R&D - or approximately 3.7% of the cost of the possible opportunities. This implies Tesla would need to spend substantially more to achieve the option value. Can tesla do it?

Summary:

The project value (S) under these scenarios range from $664 billion to $875 billion. As an analyst, you must decide if all the present incremental cash flows from the anticipated projects equal a number within this range? If so, then the market implied option may be fairly valued. If you believe the project value is too high, then the market implied option is overvalued.

The costs to exercise (X) these options range from $531 billion to $1.2 trillion. Roughly speaking Tesla has invested approximately $19.8 billion during the past 4 years. To exercise these options, the company would need to spend 27x to 63x what they have spent in the past four years to engage these projects in the next 3 years. That means they need to come up with potentially up to $1.0 trillion to meet the higher end of this range. That’s a very generous assumption, to say the least. Who would they get the money from? It would clearly need to come from outside stakeholders through a debt or equity capital raise.

My overall impressions is that the option value implied by the market is too HIGH. The present value of the cash flows from these projects is very high ($664 billion to $875 billion) given the low probability to execute on these projects within the next 3 years (autonomous vehicles, licensing technology, semi-trucks, etc.)

And I think the cost to exercise all of the projects, as implied by the market’s option value, is also too HIGH. Tesla would need to raise a substantial amount of capital.

Concluding Remarks

This style of analysis is used to make assumptions and then test their reasonableness. Do I think Tesla has option value? Yes, I do. However, using the analysis recommended in the book, I believe that the market value of the option implied by Tesla’s shareholders is too high.

The assumptions we used include a 3-year time frame. These projects may be 5-10 years away, but at that time may become highly valuable projects. We can adjust our analysis for a different time frame, volatility, etc. if we decide to do so.

The overall point is to use the analysis to understand the assumptions implied by the market so investors don’t make a mistake. I believe this style of analysis is a useful tool for all investors. Additionally, this style of analysis can help investors bridge the value and price gap as some company’s have many real options that the market may be pricing in the share price.